Now Reading: Global Trade Shock: The Panama Canal Water Crisis and the Hunt for “The Long Route”

-

01

Global Trade Shock: The Panama Canal Water Crisis and the Hunt for “The Long Route”

Global Trade Shock: The Panama Canal Water Crisis and the Hunt for “The Long Route”

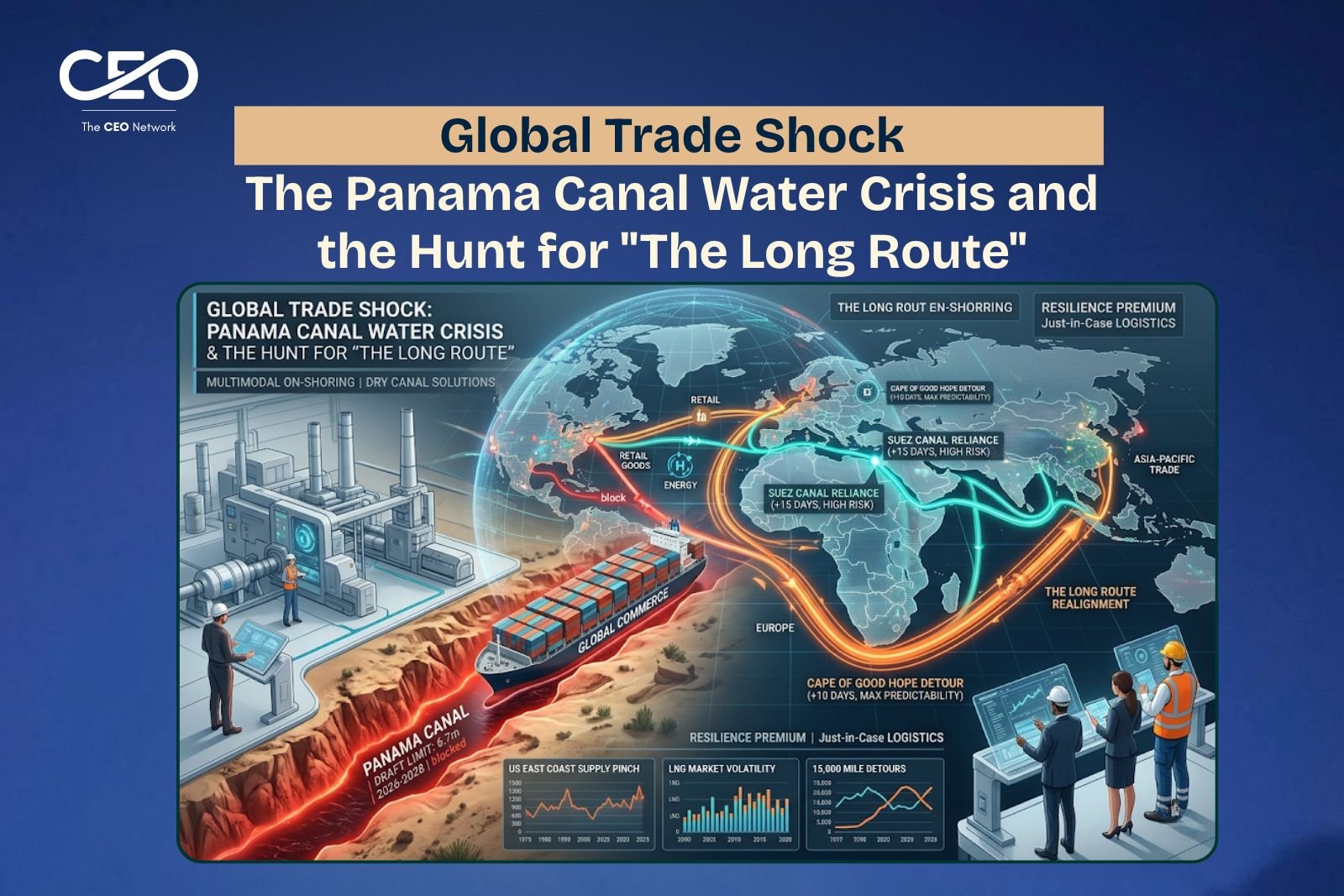

For over a century, the Panama Canal has been the apex of maritime efficiency, a 50-mile shortcut that redefined global commerce. But in 2026, climate reality has officially choked this artery. The worst drought in recorded history, fueled by persistent El Niño conditions, has turned the freshwater Gatun Lake—the canal’s crucial water source—into a shallow basin. The physical limitation is staggering: draft restrictions are severe, and daily transits have collapsed by over 60%, with no recovery forecast before Q4 2027.

For members of The CEO Network, this is not a logistical inconvenience; it is a fundamental disruption to global supply chain architecture, affecting everything from energy markets to retail inventories. This crisis has triggered a massive, complex, and permanent search for “The Long Route” as the C-suite globally executes the Great Logistics Realignment.

“We are moving beyond optimization. We are moving toward survival. Relying on a single geographical chokepoint is no longer a viable business model. The era of cheap, predictable, single-stream transit is over.”

The Multi-Channel Disruptions and the Cost Waterfall

The physical collapse of the Panama Canal’s capacity is cascading through the global economy, creating a “cost waterfall” that is reshaping pricing strategies and margin expectations.

- 1. Energy Markets: The LNG Bottleneck: The Panama Canal was the primary artery for U.S. LNG (Liquefied Natural Gas) traveling to East Asia. Now, massive LNG tankers are facing wait times of weeks or are being forced to execute a 15,000-mile detour around the Cape of Good Hope. This is driving extreme volatility in LNG spot prices and causing geopolitical realignment as Asian nations seek more secure, albeit longer, supply sources.

- 2. US Retail and Manufacturing (The East Coast Pinch): Goods bound for the US East Coast and Gulf ports are effectively bottlenecked. Retailers are facing empty shelves and exorbitant premiums for air freight, while manufacturers in the industrial Midwest are experiencing severe delays for critical components. The cost to ship a 40-foot container from Shanghai to New York has already skyrocketed by 150% in Q1 2026.

- 3. Container Congestion and Void Sailings: As lines attempt to bypass Panama, alternative ports, particularly on the US West Coast and the Suez Canal, are experiencing intense congestion. Global carriers are implementing unprecedented “void sailings” (canceling entire scheduled routes) to manage the disruption, creating massive unpredictability for global shippers.

The Great Geopolitical Shuffle: The Suez and Cape Detours

The search for “The Long Route” has elevated the Suez Canal and the Cape of Good Hope to critical, albeit complex, strategic alternates.

Alternative Routes in the Realignment:

- The Suez Canal (Increased Risk, Lower Certainty): The standard “Plan B,” the Suez Canal, has seen a 40% surge in container traffic from Asia to the US East Coast. However, the Suez remains vulnerable to geopolitical instability and physical blockage, making it an imperfect and high-risk long-term solution.

- The Cape of Good Hope (The Highest Predictability, The Longest Time): The ultimate “stable detour,” routing ships around South Africa is becoming the preferred choice for maximum reliability, despite adding 10-15 days to the journey and an estimated $1 million per vessel per transit in fuel and labor costs. CEOs are now optimizing for predictability over pure speed.

The CEO’s Panama Crisis Playbook: 2026-2030

CEOs can no longer treat logistical efficiency as a cost center. Supply chain resilience is now a board-level imperative, requiring a transition from ‘Just-in-Time’ to ‘Just-in-Case’.

Immediate CEO Actions:

- Mandate Route-Traceability Audits: By Q4 2026, identify all critical components whose supply depends on Panama or Suez transit. Demand alternative sourcing or land-bridge options from suppliers.

- Define a Logistics Diversification Budget: Formalize a “Resilience Premium.” Accept that a percentage of COGS (Cost of Goods Sold) must be dedicated to securing more expensive but reliable, multi-channel logistics.

- Invest in Multimodal Land Bridges: Look toward massive, on-shore “dry canal” solutions. The expansion of rail and road infrastructure in Mexico and the US Southwest (e.g., the expansion of the Ports of Los Angeles/Long Beach interfacing with improved rail links) is no longer optional. The land bridge is the new Panama.

The Bottom Line: Adapting to Aridity

The collapsing Panama Canal is not a temporary shock; it is the physical manifestation of an era of persistent environmental and geopolitical instability. The CEOs who win this decade will be those who recognize that efficiency can be a vulnerability. The Great Realignment requires a proactive, complex, and multi-channel approach to security. Our global trade is no longer flowing; it must be diversified, protected, and constantly redefined.

Is your organization adapting to the new arid normal, or are you still anchored to a compromised waterway?